Indian tax policy will become even more attractive for foreign companies in 2025

The Indian government wants to make it easier to do business in the country and will therefore implement important changes to the tax policy this year in order to attract more foreign investment. These changes include the exemption of foreign investors from the angel tax and a reduction of the corporate tax rate from 40% to 35%. We have listed the most important changes below.

Indian tax policy for foreign companies

Indian tax policy for foreign companies varies based on their residency status. A company’s residency status determines its tax obligations – whether the company is taxed on its worldwide income or only on income generated in India. There are two residency statuses with corresponding tax rules:

- Resident companies: According to Section 6(3) of the Income Tax Act, an Indian resident company is taxed on its worldwide income, including income earned outside of India. A company qualifies as a resident in India if:

– It is an Indian organization;

– Or if its Place of Effective Management (POEM) is in India. - Non-resident companies: Non-resident companies are only taxed on income earned, accrued or received in India. The residency status of a non-resident company is determined by the company’s turnover and its POEM. The Place of Effective Management is only considered if the company’s revenue exceeds ₹500 million or $6 million. For non-residents with revenue below this prescribed threshold, only income from India is taxed.

Reduction of Corporate Income Tax (CIT) for foreign companies

The Indian government has made a welcome move this fiscal year by reducing the corporate income tax for foreign companies in India from 40% to 35%. This tax reduction makes it easier for international companies to expand their activities in India.

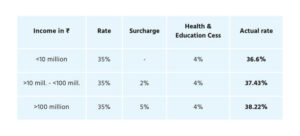

The CIT for foreign companies in India depends on their income level and is calculated as follows:

- The standard tax rate for foreign companies is 35% of the total taxable income.

- An additional surcharge of 2% is levied if the total taxable income exceeds ₹10 million but is less than ₹100 million.

- An additional surcharge of 5% is levied if the total income exceeds ₹10 million.

- Health and education tax cess: A standard surcharge of 4% is levied on the total income tax (including surcharge if applicable).

In addition, the Indian government offers marginal exemptions if the total amount to be paid – including surcharges – exceeds certain income thresholds, so that the surcharge does not place a disproportionate burden on companies.

Minimum Alternate Tax (MAT)

Foreign companies that have a permanent establishment in India are also subject to the Minimum Alternate Tax (MAT) rules. According to these rules, the company must pay a tax of 15% on the book profit if the normal tax liability is less than 15% of the book profit. However, MAT does not apply to certain types of income such as:

- Dividends

- Capital gains from the transfer of shares

- Royalties and fees for technical services

Foreign companies can avoid MAT if they are residents of countries with a double taxation agreement (DTAA) with India and they do not have a permanent establishment in India.

Goods and Services Tax (GST)

Foreign companies that supply goods or services to Indian consumers but do not have a permanent establishment in India must register for the GST. This applies to all foreign companies that are active in the Indian market, so that they comply with Indian tax legislation.

Read all about the Indian Goods and Services Tax (GST) here.

Angel Tax exemption

An important relief introduced in this fiscal year is the exemption from Angel Tax. This tax is often levied on the excess premium paid on shares by start-ups. The remission removes this burden for foreign investors, making it easier for them to invest in Indian start-ups.

What foreign companies can expect from Indian tax policy in 2025

The Indian government is expected to introduce even more flexible measures in 2025 to further stimulate business activities in India. Foreign companies should keep an eye on the following:

- Manufacturing in India will become even more attractive: The Indian government will probably continue to focus on improving India’s manufacturing capacity by expanding the Production-Linked Incentive (PLI) Scheme. This program is aimed at stimulating the production of important goods and technology within India and offers lucrative benefits for both foreign and Indian companies, especially in sectors such as electronics, textiles and the automotive industry.

- Simpler GST rates: One of the expected reforms is the merging of the 12% and 18% GST rates into a single rate, simplifying the tax structure for companies. These two rates cover approximately 70% of all taxable goods and services in India, and a uniform rate would eliminate confusion and ease the compliance burden for foreign companies.

- Amnesty scheme: To encourage companies to settle pending tax disputes, the government is expected to introduce an amnesty scheme whereby companies that voluntarily settle their pending disputes will be granted a 75% exemption from penalties. This initiative is intended to eliminate the backlog and create a more flexible and transparent tax environment. The regulation could be introduced in phases, with industries such as FMCG and textiles being given priority in the initial phase.

- Growth of the R&D sector: India lags behind the most advanced economies in the world when it comes to R&D spending, which currently amounts to only 0.7% of GDP compared to 4% in leading countries. In 2025, it is expected that some of the PLI stimulus measures will apply specifically to R&D, which could help Indian companies grow in the areas of innovation and technology. This is particularly relevant for foreign companies with R&D-focused subsidiaries or companies active in the tech industry.